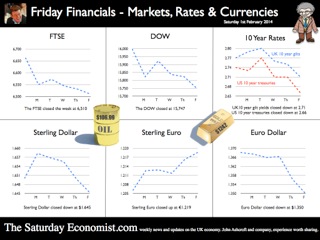

GDP growth up in the UK .. The ONS delivered the preliminary estimate of growth in the final quarter of the year this week. The UK economy grew by 2.8% year on year and 1.9% for the year as a whole. Who would believe this time last year markets were still fretting about a triple dip recession. The service sector, accounting for almost 80% of activity increased by 2.6%, construction increased by 4.5% and even the beleaguered manufacturing sector managed to push output up by 2.6%. Within the service sector, the leisure pound was once again to the fore, with strong growth in distribution, hotels and restaurants up by 4.5%. Business services increased by over 3%. We expect growth to be revised up to 2% for 2013 at some stage. For the moment we stick with our forecast of growth in 2014 and 2015 of 2.5% and 2.7% respectively. Our GDP(O) model is still performing well. The dataset has been updated and is available on the Publications page, along with our latest review of world trade. For economists, it doesn’t get more exciting. The release of the preliminary estimate is comparable to the release of a first draft of a Harry Potter chapter. What happened to the Weasleys, Gilderoy and Malfoy? Has Hagrid shaved off his beard as an end of year bet? Has Dumbledore lost weight. Has Voldemort renounced the devil and all his works? So what happened to Hermione and Harry? Can water supply and sewage really have grown by 8% in the final three months of the year? All is revealed to muggles and analysts alike by Joe Grice Chief Economist of the Office for National Statistics. In a high profile press conference, analagous to the lottery or some talent show, Joe reveals all... and the number is 1.9%. Excellent, thanks Joe. Data revisions are always interesting. But imagine if the next chapter of Rowling release revealed, the philosopher’s stone has been lost, the Chamber of Secrets has been opened to the public, the prisoner of Azkaban has been recaptured and the goblet of fire turns out to be a flaming glass of sambuca. It really can be so dramatic. After all the double dip disappeared. One day we may discover there was no recession in 2008 after all. Can’t wait for the next chapter in the GDP chronicles on the 26th February. So what happened to consumer spending and what of investment? Still stuck in the deathly hallows no doubt. US GDP also increased by 2.7% in the final quarter ... Over in the US, the Bureau of Economic Analysis announced growth of 2.7% in the final quarter and 1.9% for the year as a whole. The UK and the USA are neck an neck in the race to be the fastest growing economies in the Western World. Makes you wonder why the Fed were spending $85 million each month on treasuries and mortgage debt. No wonder the decision was made to taper further and reduce the spend to $65 billion with immediate effect. It is said that if a butterfly flaps its wings in Nicaragua, it can cause a hurricane in New York. I always found that difficult to be believe. But then who would have thought gay marriage could cause such flooding in Somerset according to UKIP. Even so, Bernanke flapping his tapering wings in Washington caused chaos in capital markets across the world. The tapering announcement led to falls in international stock markets, capital flight from developing economies and exchange rates rattling in India, Turkey and Argentina. Turkey hiked rates to over 10% to persuade the dollars to stick around. In Buenos Aires, they have long since departed. So what happened to sterling? Markets were disturbed by the decision on tapering, once again undermining stock market strength in the USA and destabilizing international capital flows across developing economies. Nevertheless, the CBOE Vix volatility index closed relatively unchanged over the week at 18.4. The pound closed at $1.6433 from $1.6481 against the dollar and 1.2184 from 1.2041 against the Euro. The dollar closing at 1.3487 from 1.3681 against the euro and 101.96 from 102.34 against the Yen. Oil Price Brent Crude closed at $106.40 from $107.88. The average price in January last year was almost $113, no real threat to inflation from crude oil prices Markets, moved down - The Dow closed at 15,698 from 15,879 and the FTSE closed at 6,5210 from 6,663. 7,000 on the FTSE no longer such a soft call for the near term. UK Ten year gilt yields closed at 2.72 from 2.78 and US Treasury yields closed at 2.65 from 2.72. Yields will test the 3% level as tapering accelerates into 2014 but for this week, once again, the flight to quality led the market. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

0 Comments

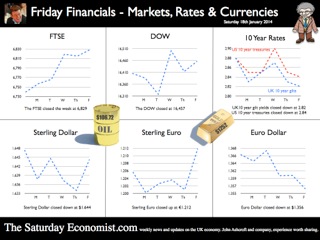

“If inflation is the genie, deflation is the ogre that must be fought decisively...” Christine Lagarde head of the IMF was speaking to the National Press Club in Washington this week. With inflation below central bank targets in Japan, USA and Europe, the IMF believe the rising risks of deflation could prove disastrous for the world recovery. Western leaders, haunted by fears of the American Great Depression and Japan’s Lost Decade, are fearful of premature monetary tightening which could threaten the nascent recovery. In folklore, a genie is a supernatural creature who does the bidding once summoned. This may not have been the intentioned meaning by the boss of the IMF but Mark Carney Governor of the Bank of England, could be forgiven the interpretation. This week, the inflation figures for December were released by the ONS. CPI inflation increased by just 2%. For the first time in over four years, the genie returned to target, as would an obedient creature, undertaking the bidding of the new Governor of the Bank of England. The genie is working hard to obey. It has taken some time to get the message into the bottle and the genie back on message! Mission accomplished? With such success, it would be churlish to point out that in the same month, RPI increased from 2.6% to 2.7%, goods inflation actually went up and service sector inflation closed the year at 2.4%. For the moment the wild ride of the last four years has come to a close. As Christine Lagarde stated, “Optimism is in the air, the deep freeze is behind us and the horizon is much brighter.” In further good news, UK manufacturing prices increased by just 1% in December and input costs actually fell by just over 1%. Import prices of metals, parts and equipment fell, reflecting higher sterling values and lower world prices. For the moment, the inflation outlook for 2014 appears benign. Deflation is the ogre ... So what of ogres and deflation. Ogres are monsters in legends and fairy tales that eat humans and are particularly cruel, brutish or hideous. In the UK fears of deflation are not evident. We still expect inflation to hover slightly above target through the year. The ogre of deflation will be banished within the Kingdom. Particularly with earnings on the rise and a Chancellor of the Exchequer, as the handsome prince, up for re election, pledging an increase in the minimum wage to £7 an hour over the next couple of years. Inflation has fallen to target much faster than we had envisaged. The good news - as earnings rise, the boost to real incomes will lead to a sustained level of growth in consumer expenditure and retail sales. Higher but not quite as high as the latest UK data might suggest perhaps! Retail Sales the nymph spirit ... This week, the ONS released the retail sales figures for December. Sales volumes increased by 5.3% and values increased by 6.1% compared to December last year. Despite the fears of the major retailers, the consumer hit the high street with great gusto in the run up to Christmas allegedly. Internet sales, increased by 11.8% and small stores, experienced higher growth with sales increasing by just over 8%. Can retail sales have been so strong in December? Contractions in volume sales amongst food stores and petrols stations adds to the confused picture in the month. According to the ONS, in the three months prior to December, retail sales volumes averaged just 2%. So much for saving for Christmas. The surge in activity in December appears rather high and slightly at odds to the anecdotal evidence from retailers themselves. The BRC, British Retail Consortium suggests sales increased by just 1.8% in December as footfall actually fell. The BDO high street tracker reported sales down in the pre Christmas week with a recovery to 3.5% growth in the final week of the year. Debenhams, M & S, Morrisons and Sainsburys struggled in the Christmas period. Argos, Dixons, Halfords, Primark, Lidl and Ocado amongst the winners in the multi channel race. The 5% growth in volumes reported by the ONS appears to be a high call. So much for lies, damned lies and seasonal adjustment. Shrek shacking up with the Sleeping Beauty ... Ogres returned to the High Street this week as Sports Direct revealed a near 5% stake in Debenhams. Imagine Shrek shacking up with Sleeping Beauty, shudders must have swept around the Debenhams board room. The subsequent put and call option by Sports Direct, just added more confusion to the retail horizon. So what happened to sterling? The pound closed at £1.6422 against the dollar and 1.2127 against the Euro. The dollar closing at 1.3538 against the euro and 104.23 against the Yen. Oil Price Brent Crude closed at $106.48. The average price in January last year was almost $113, so no real threat to inflation from crude oil prices Markets, moved higher. The Dow closed at 16,458 and the FTSE closed at 6,829. 7,000 on the FTSE a soft call for the near term. UK Ten year gilt yields closed at 2.84 and US Treasury yields closed at 2.82. Yields will test the 3% level as tapering accelerates into 2014. That’s all for this week. No Sunday Times and Croissants tomorrow or for the rest of this year for that matter. We are taking a break in this pre election year. Join the mailing list for The Saturday Economist or forward to a friend. The list is growing as is our research and our research team. John © 2014 The Saturday Economist by John Ashcroft and Company. Experience worth sharing. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.

Economics news – you don’t have to be an optimist to see the glass is half full .. Yes it's the Inflation Report “You don’t have to be an optimist to see the glass is half full”, the opening remarks from Governor Carney’s Inflation Report presentation this week. The Governor went on to say, “the glass is half full and it will be filled”. A clear reference the recovery will be allowed to gain momentum before the Bank of England and the MPC will intervene “to take away the punch bowl” and begin the rise in base rates. The MPC are sticking with forward guidance. Rate rises will not even be considered until the level of unemployment hits 7% or even lower. [Subject to caveats on inflation expectations and market stability]. When will this be? In August the Bank assumed this would be in 2016 at the earliest. On Wednesday, the Governor admitted there was a 40% chance this could be by the end of 2014 with a 60% chance it would be by the end of 2015. Such has been the strength of the economics data over the last three months. Our own models assume the knock out unemployment rate will be hit by the third quarter of 2015. Thereafter rates may rise by around 50 basis points in short time. For the moment, the MPC are on a learning journey. The path of productivity, earnings, job creation and unemployment so unclear, we are all embarking on a “learning journey” suggested the governor. The £5m recently spent on the Bank of England model, of little value in the new world it would appear. Charlie Bean appeared most discomfited by the trip. Economics from Cambridge, a PhD from MIT and teaching at Stanford and LSE in the knowledge pack. One could be forgiven the reluctance to take the Mark Carney refresher course. But then why not? Having seriously failed to understand the impact of low rates on investment and depreciation on the trade balance, it is time to denounce the omniscient stance of the Oxbridge collective. Yes send them back to school. Martin Weale was indeed sent back to school this week. The MPC member was delivering a speech on the role of monetary policy and forward guidance to A-level students in London. “To cut a long story short, our job is to ensure that people buy coats when they need them”. Excellent. I am sure that cleared things up. Martin once worked in a shop apparently. Yes the black cloud gang disbanded, it’s back to school for all. Fill up your glasses, the punch bowl is on the table, the Carney Credit card is behind the bar. Inflation Good news for the Governor, inflation fell in October CPI to 2.2% from 2.7% in the prior month. Education hikes last year fell out of the index as we expected but the fall in transport costs pushed the index even lower. 2.4% CPI inflation was our call and still seems to be a reasonable target by the end of the year. Manufacturing prices suggest there is little cost pressure in the economy but retail energy prices are moving significantly higher. Retail Sales Retail sales figures in October were slightly disappointing, an increase of 1.8% in volume and 2.5% in value, slightly down on the averages in Q3. The demise of Barratts Shoes and Blockbuster a reminder, conditions remain tough on the high street as household real incomes remain under pressure. Internationally Janet Yellen, the new head at the Fed is still worried about the strength of the US recovery. Tapering may be postponed still later into the New Year. Growth in France and Japan in the third quarter a further warning the world recovery still requires accommodation. QE tapering US style is not the answer. Buying treasuries and Mortgage Backed Securities to support asset prices makes no sense. Blend a NASDAQ tracker fund into the purchase mix would follow the logic and demonstrate the folly. What happened to sterling? Sterling closed at £1.6113 from £1.6018. Against the Euro, Sterling closed at €1.1940 from €1.1982. The dollar moved up against the yen closing at ¥100.1 from ¥99.1 and closing at 1.3494 from 1.3368 against the Euro. Oil Price Brent Crude closed at $108.50 from $105.12. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,962 up from 15,762. The FTSE closed at 6,693 from 6,708. UK Ten year gilt yields closed at 2.75 from 2.77 US Treasury yields closed at 2.70 from 2.75. Yields will test the 3% level over the coming months. Gold closed at $1,288 from $1,284. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.

Economics news – import drive and the march of the makers ...

Import Drive ... “Sales of European cars drive trade gap wider” is the headline in the Times today as Britons “flocked” to buy cars built on the continent. The trade figures released this week, reveal the September deficit (trade in goods) increased to £9.8 billion from £9.6 billion last month. The trade deficit with the EU reached a record £6.0 billion as imports increased by £0.4 billion to £18.6 billion. “Half of the increase is attributed to cars”, according to the ONS, hence the slightly unbalanced headline from the Times. In reality, Britons have been flocking to the showrooms since the start of the year. Car sales are up by 10% this year. The deficit was offset as usual by a trade in services surplus of £6.5 billion. This is a familiar pattern which should come as no surprise to readers of The Saturday Economist. The trade deficit will deteriorate further especially if the UK continues to grow at a faster rate than major trading partners in the EU and USA. We are forecasting an overall trade deficit this year of £110 billion offset by a service sector surplus of almost £80 billion. The residual overall deficit easily financed. The September figures are confirmation of the trends within our well established trade model. Depreciation damages UK trade in goods performance. Imports do not react significantly to price changes. There will be no rebalancing of the economy. March of the makers picks up pace ... Did the march of the makers pick up the pace in September? Not really. According to the latest figures from the ONS. Manufacturing output increased in the month by just 0.8%. Output for the quarter was flat as signaled in the Markit/CIPS PMI® survey data last week. Nevertheless we still expect manufacturing growth of almost 2.5% in the final quarter of the year. Last year was such a dismal quarter, even the stumbling marchers will make progress. Watch out for the headlines heralding the rebalancing over the next few months and tie me to a chair. Other survey news ... The service sector continues to drive growth in the economy according to the Markit/CIPS UK Services PMI® for October. The headline Business Activity Index reached a level of 62.5 in October. “The UK service sector maintained its recent run of strong growth during October, with activity expanding at the fastest pace since May 1997 as levels of incoming new business rose at a survey record rate”. The construction rally also continues according to the Markit/CIPS UK Construction PMI® index. The sharp rebound in UK construction output continued in October. The lead index posted 59.4, up from 58.9 in September, above the 50.0 no-change threshold for the sixth consecutive month. So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. The pick up in manufacturing output will add to the growth in services and construction. Higher growth, more jobs, lower borrowing, inflation falling, investment will pick up in the second half of next year, it’s all looking pretty good for the Chancellor. Just the trade figures will continue to disappoint. We now think base rates are now more likely to rise by around 50 basis points in 2015. Higher growth will result in unemployment hitting the 7% hurdle rate in the third quarter of 2015, several months after the election. What happened to sterling? The Euro rate cut weakened the hybrid and Sterling strengthened as a result. The pound closed at £1.6018 from £1.5912. Against the Euro, Sterling closed at €1.1982 from €1.1814. The dollar moved up against the yen closing at ¥99.1from ¥98.7 and closing at 1.3368 from 1.3484 against the Euro. Oil Price Brent Crude closed at $105.12 from $105.91. The average price in November last year was almost $110. We expect Brent Crude to average $110 in the month, with no material inflationary impact. Markets, pushed higher - The Dow closed at 15,762 up from 15,616. The FTSE closed at 6,708 from 6,721. The rally continues with a stronger Santa rally in prospect over the next five weeks. UK Ten year gilt yields closed at 2.77 from 2.66 US Treasury yields closed at 2.75 from 2.62. Yields will test the 3% level over the coming months. Gold closed at $1,284 from $1,312. The bulls may have it may just have to wait for now. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow and watch out for news of our Friday Financials Feature with Monthly Markets updates coming soon. John Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist.  Economics news – news from Washington and Beijing ...

Washington Good news from across the Pond, a Washington truce has been achieved. The US government has returned to work, Yosemite National Park is open, international creditors will be paid. The debt crisis is over. A twenty week truce has been secured. Markets rallied, the dollar slipped, Google shares breached the $1,000 level and the S&P 500 hit a new high. What more could we ask? Beijing In China, growth continued at 7.8% into the third quarter up from 7.5% in the second. For those fearing a hard landing, crash landing, soft landing, end of the world scenario, it is time to stop shorting the markets and buy in, the world is not coming to an end any time soon. London - Mortgages In the UK, mortgage lending increased by 32% in the third quarter compared to Q3 last year. FLS and Help to Buy are boosting the market. We expect house prices to rise by 5% this year and almost 8% next year before a normalized escalation returns. Prices are beginning to rise across the UK. Yes Prices will move across the UK, like a tidal wave across the flood plain. Check out The Saturday Economist Housing Market Review for more information. Inflation Tuesday, the ONS released the latest inflation figures for September. CPI inflation was unchanged at 2.7% as RPI moved down slightly to 3.2% from 3.3%. We expect a further fall in CPI inflation around 30 basis points next month, as education fees drop out of the data series. Thereafter prices will be pretty sticky around 2.5%. Energy costs are set to rise and service sector inflation at 3.4% up from 3.0% last month will create problems for policy makers. As we have long pointed out, service sector inflation has averaged 3.7% for the last twenty years. Manufacturing prices Manufacturing Prices, on the other hand, have averaged around 1% over the same period, boosted by falls in clothing and footwear specifically. The immediate outlook for manufacturing prices is pretty benign, Output prices increased by just 1.2% in September and input costs increased by 1.1%, down from 5% in July. Retail sales Retail sales were also released this week. Retail sales volumes were up by 2.2% in September and by 2.4% in the third quarter. Sales values increased by almost 4% in the three months boosted by on line sales and department store sales. Is the housing market stimulating footfall? Quite probably. We expect the volume of housing transactions to increase significantly this year, boosting sales of carpets, furniture durables and DIY goods in the process. Employment The employment figures were also released this week. The claimant count fell by over 40,000 in September to a rate of 4% compared to 4.2% last month. The wider FLS count fell in the three months to August, to 2.87 million, a rate of 7.7% from 7.8% last month. Lagging as it does, the broader unemployment rate could fall to around 7.5% by the end of the year. The Bank of England “knock out rate” under forward guidance at 7% could be in sight by the end of 2014. So what of base rates? Interesting Spencer Dale the Bank of England’s chief economist was on Twitter this week in a hashtag #AskBoE “open hour” adventure. The telling tweet - a rate rise in 2014 was unlikely. Just as unlikely as a rate rise in 2016 no doubt. The markets expect a move in 2015 but will it wait until after polling day? We will have to ask next time the bank is online, perhaps using Facetime or Skype? What would Governor King have made of it all! So what does this all mean? The economy is recovering and growing at a much faster rate into the final quarter. The first estimate of GDP in Q3 will be released next week. We expect growth year on year to be over 1.5% rising to trend rate in the final quarter of the year. Inflation is falling, employment is rising, even the debt figures due next week will look much better. Energy costs may provide a problem for households but “wear a jumper”, the ministerial advice could keep bills down and boost retail sales in the process. What happened to sterling? Sterling moved up against the dollar and against the Euro as the dollar slipped. The pound closed at £1.6174 from $1.5954. Against the Euro, Sterling closed at €1.1816 from €1.1772. The dollar moved down against the yen closing at ¥97.7 from ¥98.5 and closing at 1.3682 against the Euro. Oil Price Brent Crude closed at $109.94 from $111.28. The average price in October last year was almost $112. We expect oil to average less than $112 in the month, with no inflationary impact. Markets, pushed higher - The Dow closed at 15,399 up from 15,237. The FTSE closed at 6,623 from 6,487. The US debt deal is done. The rally is on. UK Ten year gilt yields closed at 2.72 from 2.74, US Treasury yields closed at 2.58 from 2.69. Gold closed at $1,313 from $1,270. The bulls have it, at least for the week. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or please forward to a colleague or friend. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below. If you enjoy the content, why not forward to colleague or friend.  Good news for the economy continued this week.

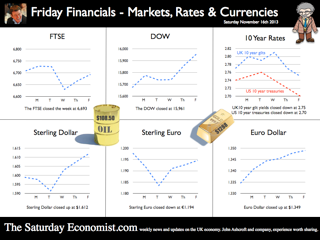

A fall in the rate of unemployment AND an increase in output and orders for the construction industry. Who would believe it was just a few months ago headlines were devoted to the risk of a triple dip recession? The year is becoming a tale of two halves with a significant pick up in activity and sentiment into the third quarter. Get ready, we are leaving Planet ZIRP. Speed bumps in the housing market It is a strange recovery with strange roles in evidence. The Bank of England is hoping to keep base rates on hold for three years. The RICS warned this week of the need to maintain a stable and sustainable path for house prices. “We suggest setting an annual growth rate threshold in a national index, which if exceeded, triggers tighter macro prudential policy” said Josh Miller Senior Economist in the RICS report. The RICS is advocating “speed bumps” to limit the rate of price increases. The Bank of England (in the form of the FPC) should intervene to regulate mortgage allocations of LTV ratios across the UK if prices moved over 5%. That sort of thing. “Taking away the punch bowl as the party gets started” is the traditional role of the central banker. Now some of the heavy drinkers are suggesting, we dilute the hooch. How strange. Most commentators have reacted badly to the suggestion. Why 5%? Is there a regional variation? Is it the same for maisonettes and mansions? Should the government confiscate revenues where prices exceed the guidelines? Are the RICS advocating a prices and incomes board, monitored by the RICS perhaps? Graeme Leach at the IOD has suggested it is a “statist solution to a state created problem”. Calm down Graeme, it was just for fun and not to be taken too seriously. The FPC is to meet this week. Top of the agenda will be the need to limit loan to value ratios. The government “homes for heroes” scheme, (the scheme in which the tax payer underwrites high loan values for house buyers) will be on the agenda no doubt. Unemployment The unemployment rate ticked down in July to 7.7% in July. The claimant count fell to 4.2% in August. The number of claimants - down by 32,000 to 1.4 million. Further indicators the recovery is on track, towards trend rate of growth, into the final quarter. What does this mean for forward guidance? The models still suggest it will be the end of 2015 at least before the 7% threshold will be reached. That is the rate at which the MPC will begin to think about base rate rises, (speed bumps and knock out drops aside). The caveat about earnings continues. The recovery cannot be sustained without a change in household fortunes, either lower inflation or higher earnings growth is required. Plus, the UK cannot grow at a faster rate then Europe for too long, without the trade deficit coming under severe pressure. The trade deficit, of itself, “a speed bump or pothole”, where growth is concerned. Construction Good news on construction. Output increased in July by 2% compared to July last year. Orders for new work, especially in the housing market, were up by 33% compared to the same time last year. This is an important change indicator for the sector. Overall the growth in services continues. The recovery in manufacturing and construction will look much stronger into the final quarter of the year. The UK recovery is on track. It is just over eighteen months to the election. Buckle up, we are leaving Planet ZIRP. Gilts are already in low orbit. What happened to sterling? Sterling responded to the economics news, moving up against the dollar and also against the Euro. The pound closed at $1.5871 from $1.5627 and at €1.1940 from €1.1860 against the euro. The dollar moved up against the yen closing at ¥99.4 from ¥99.0 Oil Price Brent Crude closed at $111 from $114. The average price in September last year was almost $113. We expect oil to average $112 in the current quarter, with no real inflationary impact. Markets, rallied - The Dow closed up at 15,376 from 14,923. The FTSE closed up at 6,584 from 6,547. The Fed statement this month will mark the larger DOW move. Still a good time to move in? The FTSE will clear 7000 within ten weeks and the DOW will press 16,000. UK Ten year gilt yields closed at 2.94 from 2.95, US Treasury yields closed at 2.89 from 2.93. Long rates are decoupling from shorts, returning to fair value. They are just a bit reluctant to leave! Gold closed at $1,312 from $1,388. The bulls have it or do they? Some still worry about tapering. That’s all for this week, don’t miss The Sunday Times and Croissants out tomorrow. Join the mailing list for The Saturday Economist or forward to a friend UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John © 2013 The Saturday Economist. John Ashcroft and Company, Dimensions of Strategy . The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice.  Economics news – don't get carried away with survey data ...

The week started well but ended on something of a whimper. The highly rated Markit/CIPS PMI® series reported this week with strong updates on manufacturing, construction and services. The manufacturing index hit a two year high of 57.2 as output grew at the fastest rate since 1994. The construction output index increased at the fastest rate since 2007 to a level of 59.1.The service sector grew at the fastest rate since December 2006, as the headline index increased to 60.5. The Saturday Economist weighted index closed at 60.0 suggesting strong growth, around trend rate, in the economy overall. Good news? Of course but survey data should always be treated with a little caution. It’s hard to believe just a few months ago, markets were concerned about a triple dip recession, relying, as they will, on shot run runes. OECD and NIESR The OECD added to the impetus suggesting growth in the UK will be 1.5% this year rising to 2.5% in 2014. The NIESR monthly GDP tracker for August released this week, implied the economy is growing at a rate of 1.5% in the third quarter. House Prices The Halifax House Price Index reported house prices increased by 5.4% in August. As Martin Ellis, Housing economist at the lender explained, “Economic improvement and low interest rates, supported by official schemes such as Funding for Lending and Help to Buy, appear to have boosted housing demand in recent months”. Quite! Payroll Friday It was all looking pretty good until “Payroll Friday”. The US jobs data proved something of a disappointment to markets. The US economy added 169,000 jobs in August as the unemployment rate remained relatively unchanged at 7.3%. Is that so bad? Not really, the US is on track for growth of almost 2% in 2013. It’s a recovery of sorts and probably just enough for the Fed to stop tampering and begin tapering later this month. In the UK, a further setback for those who ever believed in the march of the makers, rebuilding the workshop of the world and rebalancing the economy in the process. Are there any left? Manufacturing output fell in July by just under 1% and the trade balance slumped to a deficit of just under £10 billion. Hardly a recipe for strong growth this year. Manufacturing output will be better in the second half of the year but we see little contribution to output for the year as a whole. The deficit (trade in goods) will be around £106 billion, providing a significant drag on net growth. For the moment we are sticking with our growth forecast of around 1.2% for the year rising to over 2% in 2014. The rate of growth in the second half will be stronger but the legacy of the first six months is a great drag on output for the year. It could be time to upgrade the forecast for next year towards trend rate 2.4%. What happened to sterling? Sterling responded to the economics news, moving up against the dollar and also against the Euro. The pound closed at $1.5627 from $1.5494 and at €1.1860 from €1.1719 against the euro. The dollar moved up against the yen closing at ¥99.0 from ¥98.1 Oil Price Brent Crude closed up at $116 from $114. The average price in September last year was $113. We expect oil to average $112 in the current quarter. Markets, rallied - The Dow closed up at 14,923 from 14,810. The FTSE closed up at 6,547 from 6,413. The Fed statement this month will mark the DOW move. A good time to move in? The FTSE will clear 7000 within ten weeks and the DOW will press 16,000. UK Ten year gilt yields closed up at 2.95 from 2.79, US Treasury yields closed at 2.93 from 2.79. Long rates are decoupling from shorts, returning to fair value. Gold closed at $1,388 from $1,394. The bulls have it or do they? That’s all for this week, If you enjoy the Saturday Economist, why not forward to a colleague of friend. Here's is the link to join the Mailing list for The Saturday Economist. John 10,000 now receive the Saturday Economist each week. UK Economics news and analysis : no politics, no dogma, no polemics, just facts. John Ashcroft is the Saturday Economist, Chief Economist at the Greater Manchester Chamber of Commerce, Economics Adviser to Duff & Phelps and Chief Executive of pro.manchester. The views expressed are personal and in no way reflect the policy statements of organisations with which we work. The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of investment advice. It's just for fun, what's not to like! Dr John Ashcroft is The Saturday Economist. |

The Saturday EconomistAuthorJohn Ashcroft publishes the Saturday Economist. Join the mailing list for updates on the UK and World Economy. Archives

May 2024

Categories

All

|

| The Saturday Economist |

RSS Feed

RSS Feed

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The presentation should not be construed as the giving of investment advice.

|

The Saturday Economist, weekly updates on the UK economy.

Sign Up Now! Stay Up To Date! | Privacy Policy | Terms and Conditions | |